Weekly Treasury Market Recap: 2-, 5- & 10-Year Yields Respond to Data and Risk

As markets transitioned into the first full trading week of 2026, the U.S. Treasury complex saw meaningful intra-week movement across the 2-, 5- and 10-year maturities, reflecting the market’s evolving view on interest rates, incoming economic data, and geopolitical risk.

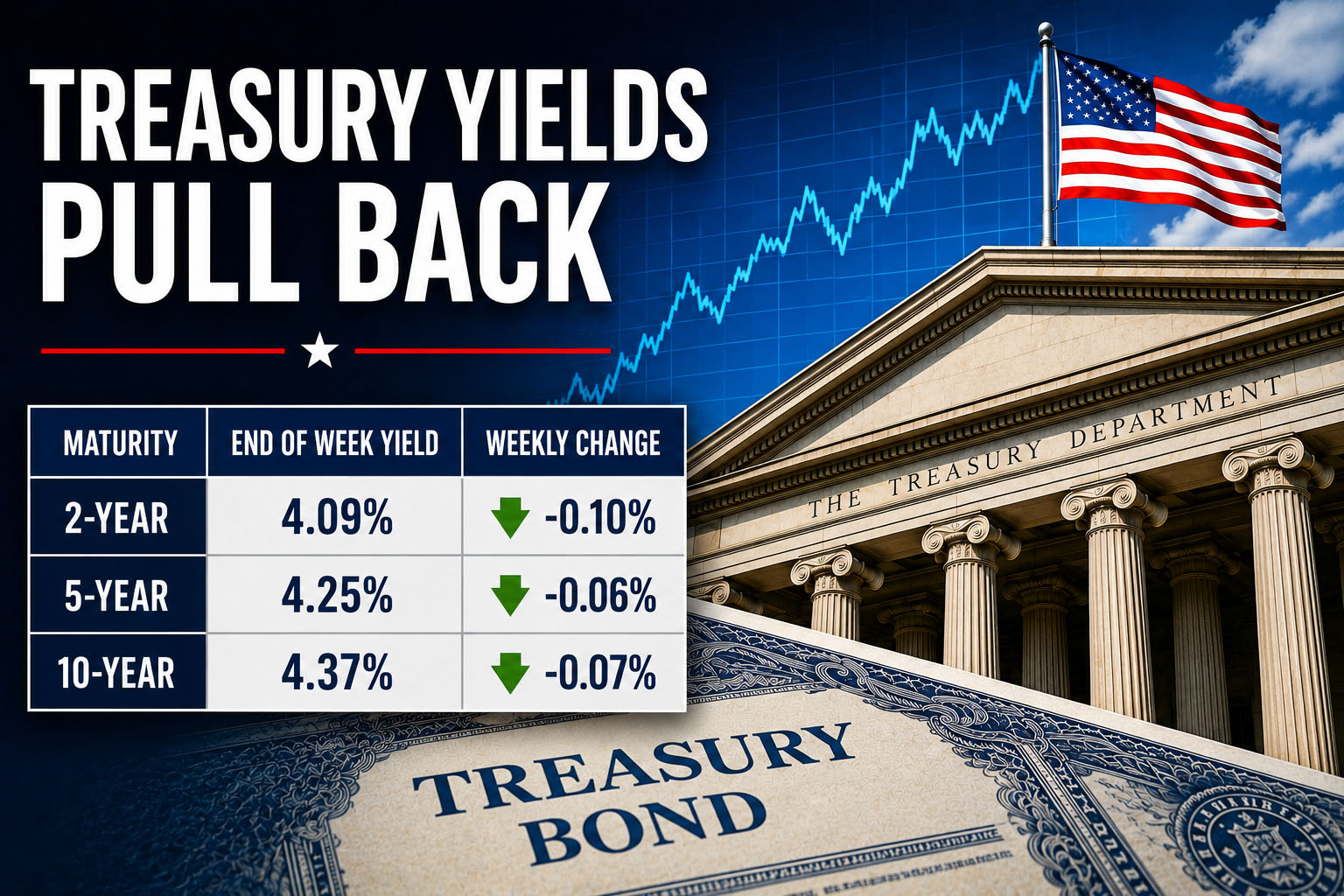

Where Yields Traded

By Friday, January 9, 2026:

- 2-year Treasury yield finished near ~3.54%.

- 5-year yields held around the mid-3.7% area.

- 10-year Treasury yields closed around ~4.18%.

These levels represent modest swings over the week but with distinct directional nuance across the curve. Federal Reserve+1

Put simply:

- Shorter maturities (2-year) bumped higher in response to data that sustained market expectations for sticky rates.

- Intermediate (5-year) and longer (10-year) tenors fluctuated on risk sentiment and inflation expectations.

What Drove These Moves

1. December Jobs Report (Economic Data)

The standout macro event was the December 2025 employment report — where the U.S. economy added only ~50,000 jobs, well below expectations, even as the unemployment rate ticked down to 4.4%. Reuters+1

Market interpretation:

- Soft payrolls reinforced views of slowing labor market momentum.

- The slight improvement in unemployment, however, suggested labor market resilience, leaving traders less confident that the Fed would cut rates imminently.

In practice, this pushed:

- 2-year yields up modestly, as markets dialed back aggressive rate-cut pricing,

- 10-year yields slightly lower or stable, as long-duration Treasuries benefited modestly from safe-haven demand and more balanced growth expectations.

That dynamic — front-end up, back-end steady or slightly lower — effectively flattened sections of the curve on data that muddled the policy outlook.

2. Equity and Risk Appetite

Equities rallied to fresh record highs by Friday, buoyed in part by the jobs data interpreted as soft enough to allow easier policy over time but not so weak as to signal recession. AP News

Why this matters for Treasuries:

- Equity strength can pull yields higher, particularly at the front and belly of the curve, as risk assets attract flows away from safe bonds.

- But the absence of clear near-term cuts limited aggressive sell-offs in longer yields.

3. Geopolitical and Policy Uncertainty

Though no single headline geopolitical shock dominated this past week, broader tariff policy uncertainty and anticipation of political/legal events remained a background theme for markets. Fidelity Fixed Income

Uncertainty about the Supreme Court ruling on tariff legality contributed to bouts of caution in the fixed income market, with some Treasury yields falling on news of softer macro data and rising on risk repricing ahead of rulings and policy announcements.

Geopolitical Risk and Safe-Haven Dynamics

Treasury yields are influenced not only by domestic data but also by global risk sentiment. In periods of heightened geopolitical tension, long-dated yields often fall as investors seek safety, while risk appetite can push shorter yields around rate expectations.

This interplay — especially among the 5- and 10-year maturities — has been observable over recent months and was present this week though muted. Reuters

Interpreting the Treasury Curve

As of this week, the yield curve remained normal/slightly positively sloped (with longer yields above shorter ones), albeit with front-end sensitivity to policy expectations. StreetStats

This pattern suggests:

- Markets still expect economic growth above recessionary thresholds,

- Inflation pressures have not fully receded,

- And monetary policy isn’t priced to pivot sharply in the very short term.

This is a classic mixed signal environment from the market’s perspective.

Key Drivers to Watch in the Coming Week

1. More High-Frequency Data

With labor market conditions remaining in focus, traders will watch early January data releases (like weekly jobless claims and PMI surveys) for confirmation of the December trend.

Such data could swing both short and intermediate rates meaningfully:

- Stronger data → higher front-end yields (less chance of cuts),

- Weaker data → lower long yields (softer growth outlook).

2. Inflation Signals

Inflation remains a main driver for longer maturities. Any reacceleration in core inflation data (CPI, PCE) would tend to push 5- and 10-year yields higher, compressing yield spreads further.

Conversely, soft inflation prints may heighten demand for longer duration.

3. Geopolitical Developments

While no major conflict shock dominated this week, ongoing global risk factors — trade negotiations, sanctions, or Middle East tensions — can rapidly reshape long yield curves if safe-haven demand spikes again.

Bottom Line

This past week’s Treasury yield behavior — 2-year bump on policy uncertainty + mixed jobs data, intermediate/longer tenors stable or slightly lower — tells a story of markets still balancing growth expectations, inflation trends, and the timing of future Fed action.

With mixed macro prints, ongoing political/legal events, and lingering geopolitical risk, Treasury yields look poised for continued intraday and interday volatility in the coming sessions.

This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. ©2026 MIXED MARKET ARTIST

(Visit Fin Pro Marketing – The Best Marketing for Finance Professionals)