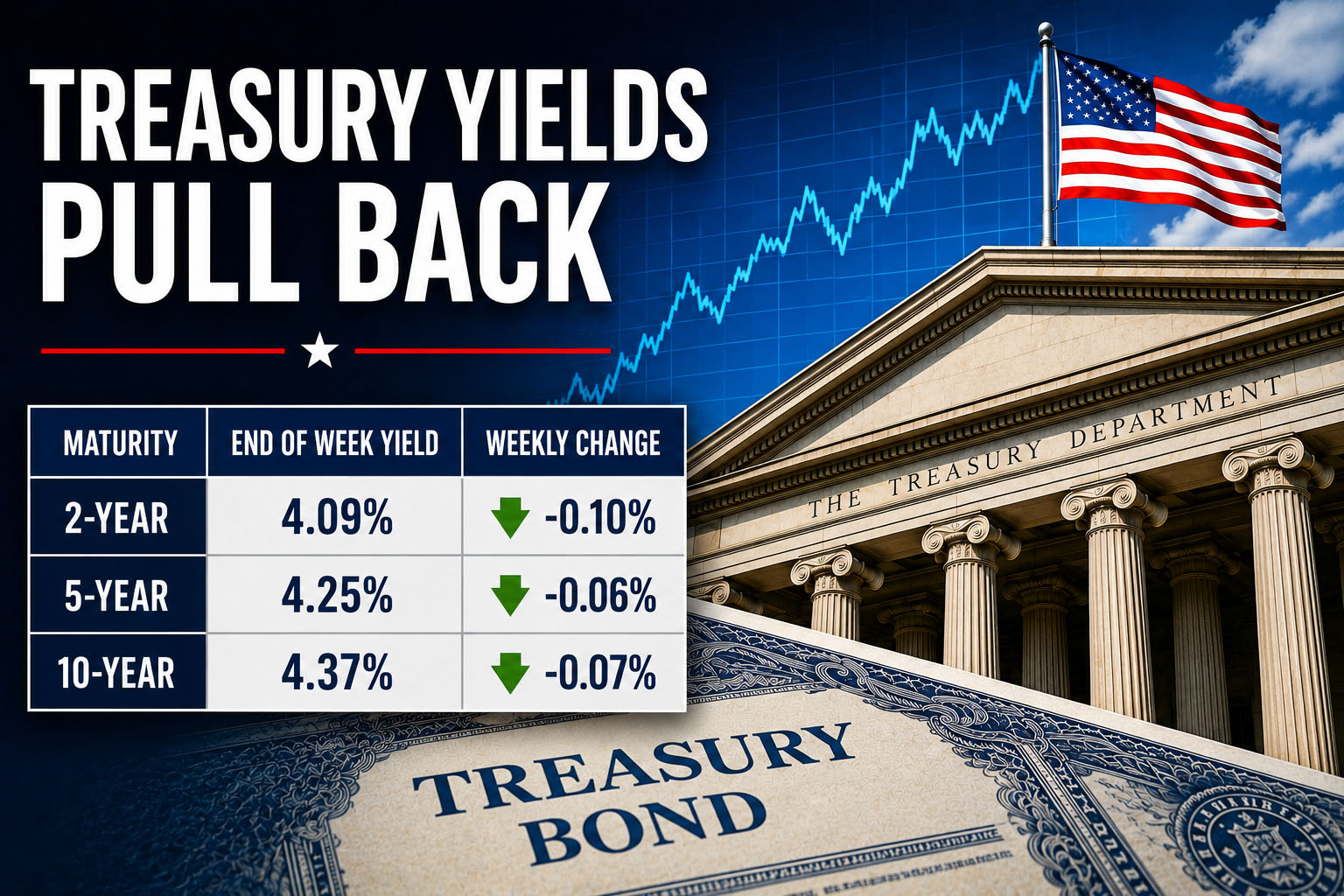

Treasury Rates This Past Week: 2s, 5s, and 10s Moved Lower, Then Rebounded Into Friday

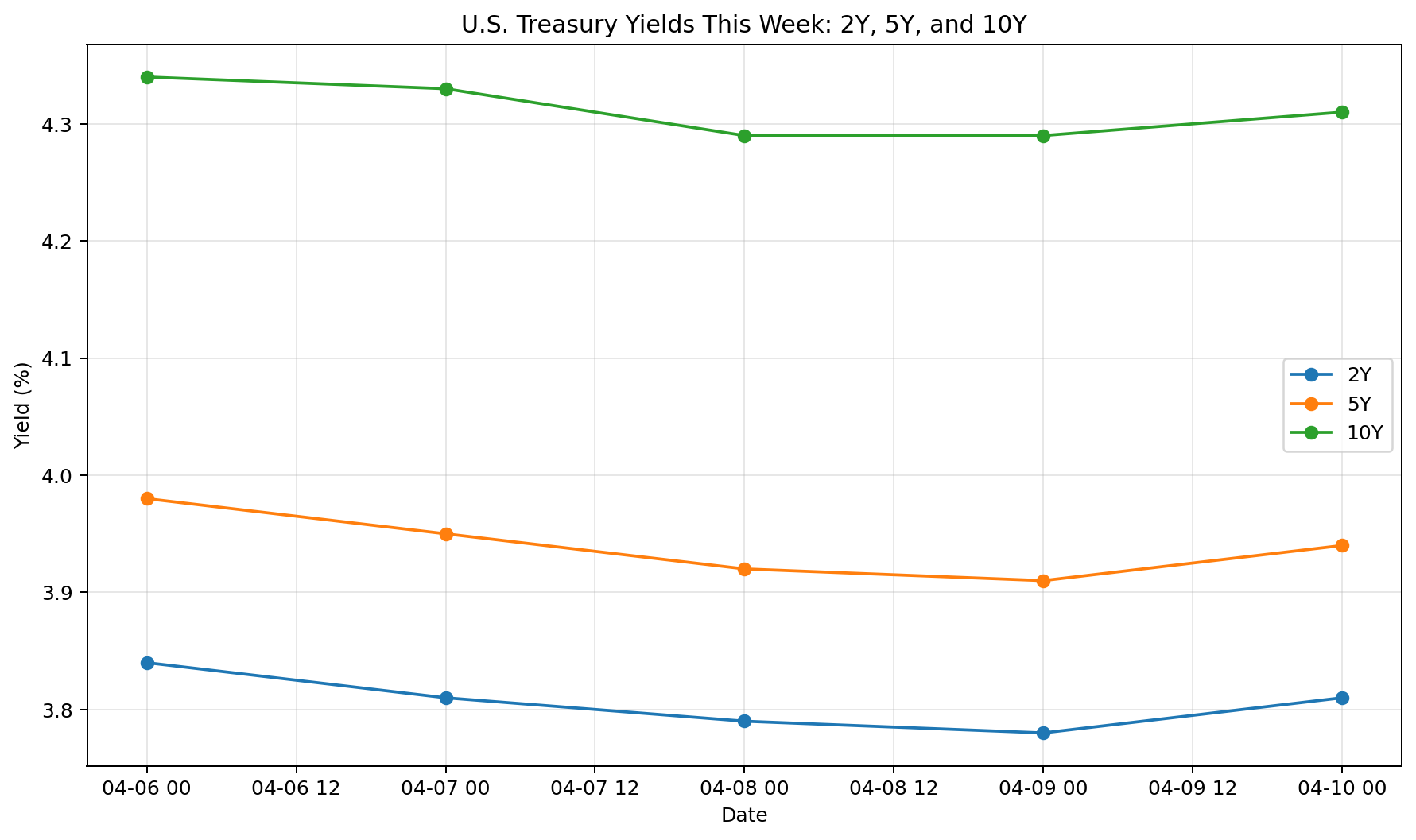

U.S. Treasury yields spent most of the week drifting lower before firming modestly into Friday. From Monday, April 6, to Friday, April 10, the 2-year yield moved from 3.84% to 3.81%, the 5-year from 3.98% to 3.94%, and the 10-year from 4.34% to 4.31%. Midweek, yields fell more noticeably as the market reacted to a temporary U.S.-Iran ceasefire and a sharp drop in oil prices, which eased some of the immediate inflation fear that had been building around energy markets. By Thursday, the 2-year had slipped to 3.78%, the 5-year to 3.91%, and the 10-year to 4.29%, before all three edged back up on Friday.

The weekly pattern mattered more than the final Friday move. Early in the week, the bond market treated the ceasefire headline as disinflationary. Reuters reported that Brent crude fell 13.29% to $94.75 and WTI dropped 16.41% to $94.41 after the ceasefire announcement, as traders started to price in reduced odds of a prolonged energy supply shock through the Strait of Hormuz. That helped pull longer-dated Treasury yields down as inflation expectations cooled and growth fears softened.

By the end of the week, however, the market had to digest the March CPI report. The Bureau of Labor Statistics said headline CPI rose 0.9% month over month and 3.3% year over year in March, up from 2.4% year over year in February. Core CPI rose 2.6% over the prior 12 months. That headline inflation jump, driven heavily by energy, was hot enough to keep the Fed from sounding comfortable, but the softer core reading helped prevent a much bigger selloff in Treasuries. That is why yields rose only slightly on Friday instead of breaking sharply higher.

Looking across the curve, the move was mostly a lower parallel shift through midweek, followed by a small Friday backup. The 2s-10s spread was about 50 basis points on Monday and remained around 50 basis points on Friday, so this was not a dramatic steepening or flattening story. It was more of a geopolitical and inflation repricing story, with the whole intermediate part of the curve pulled down as oil collapsed, then nudged higher again when investors refocused on still-uncomfortably-high headline inflation.

The 2-year yield remained the cleanest read on Fed expectations. It fell from 3.84% on April 6 to 3.78% on April 9, then rebounded to 3.81% on April 10. That says the market briefly leaned toward a less hawkish Fed path when the ceasefire reduced near-term inflation pressure, but it was not willing to fully look through a 3.3% CPI print. The 5-year and 10-year traced a similar pattern, though the 10-year’s move also reflected shifting views on growth, term premium, and geopolitical risk.

What drove rates this week

The biggest geopolitical driver was the Middle East. A temporary U.S.-Iran ceasefire announcement helped push oil sharply lower and pulled yields down midweek. But by the weekend, Reuters reported that talks in Islamabad had failed to produce a breakthrough, renewing concerns that the ceasefire is fragile and that energy-market stress could return. That matters for Treasury yields because the bond market is now trading not just U.S. growth and Fed policy, but also the probability that oil shocks keep bleeding into inflation data.

The biggest economic driver was inflation. March CPI confirmed that the energy shock made it into the official data. Even though core inflation was somewhat better behaved, the bond market could not ignore a headline print of 0.9% month over month. Friday’s modest rise in yields reflected that tension: inflation was bad enough to keep rate-cut hopes in check, but not bad enough to overwhelm the relief coming from lower oil prices and a calmer, if still unstable, geopolitical backdrop.

What could move Treasury rates next week

The next scheduled macro test is the March Producer Price Index on Tuesday, April 14, at 8:30 a.m. Eastern. PPI matters because it will show whether pipeline price pressure is broadening beyond the consumer energy spike. Import and export price indexes follow on Wednesday, April 15, and the Fed’s industrial production report is due Thursday, April 16. Those releases will help shape the market’s read on whether the economy is absorbing the recent shock or beginning to slow under it.

One wrinkle for the week ahead is that some widely watched data will not arrive on the usual timetable. The Census Bureau says the March 2026 retail sales release, originally set for April 16, was pushed back to April 21. It also says the March housing starts report, originally scheduled for April 17, was rescheduled to April 29. That means rates next week may be even more sensitive than usual to inflation releases and geopolitical headlines because two important growth indicators are not on the board yet.

Politically, the bond market will stay locked onto the U.S.-Iran situation. Reuters reported on April 12 that talks faltered and ceasefire doubts resurfaced. If those talks deteriorate further and oil turns back up, Treasury yields could rise again, especially in the 5-year and 10-year tenors where inflation expectations and term premium matter most. If diplomacy stabilizes and energy prices continue to ease, the market may feel more comfortable bringing yields lower again, particularly if PPI does not show another inflation surprise.

Bottom line

The 2-year, 5-year, and 10-year Treasury yields all finished the week modestly below Monday’s levels, but the path was anything but calm. Rates fell as the Iran ceasefire knocked down oil and reduced immediate inflation pressure, then firmed into Friday as CPI reminded investors that the inflation problem has not gone away. Next week, PPI, import prices, industrial production, and any new Middle East headlines will be the main drivers. For now, the Treasury market is trading the same question every day: was March’s inflation surge a temporary energy shock, or the start of a broader reacceleration that keeps yields higher for longer?

Sources

- U.S. Department of the Treasury

Daily Treasury Par Yield Curve Rates

https://home.treasury.gov/resource-center/data-chart-center/interest-rates - Board of Governors of the Federal Reserve System

H.15 Selected Interest Rates (Daily Treasury Yields)

https://www.federalreserve.gov/releases/h15/ - U.S. Bureau of Labor Statistics

Consumer Price Index – March 2026

https://www.bls.gov/cpi/ - U.S. Bureau of Labor Statistics

Producer Price Index (Release Calendar and Data)

https://www.bls.gov/ppi/ - U.S. Bureau of Labor Statistics

Import and Export Price Indexes

https://www.bls.gov/mxp/ - Federal Reserve

Industrial Production and Capacity Utilization

https://www.federalreserve.gov/releases/g17/ - U.S. Census Bureau

Advance Retail Sales and Housing Starts Release Schedules

https://www.census.gov/economic-indicators/ - Reuters

Coverage of U.S.–Iran Ceasefire, Oil Markets, and Global Risk Sentiment

https://www.reuters.com/

(Visit Fin Pro Marketing – The Best Marketing for Finance Professionals)

Billy Lee, CEO of Great White Financial, is a sportsman, businessman, artist, speaker, writer, and producer.

Billy is the Founder of the Wellness Institute for Economic Growth and Kairos Athletics.