Treasury Yields Pull Back as Geopolitics Cool and Inflation Stays Contained

After several weeks of volatility driven by geopolitical tensions and shifting Federal Reserve expectations, U.S. Treasury yields finished this past week lower across much of the curve.

While the moves were not dramatic, they reflected an important change in market psychology: investors became less concerned about an immediate inflation shock from geopolitical events and increasingly focused on incoming economic data.

Weekly Treasury Performance

Approximate weekly closing levels:

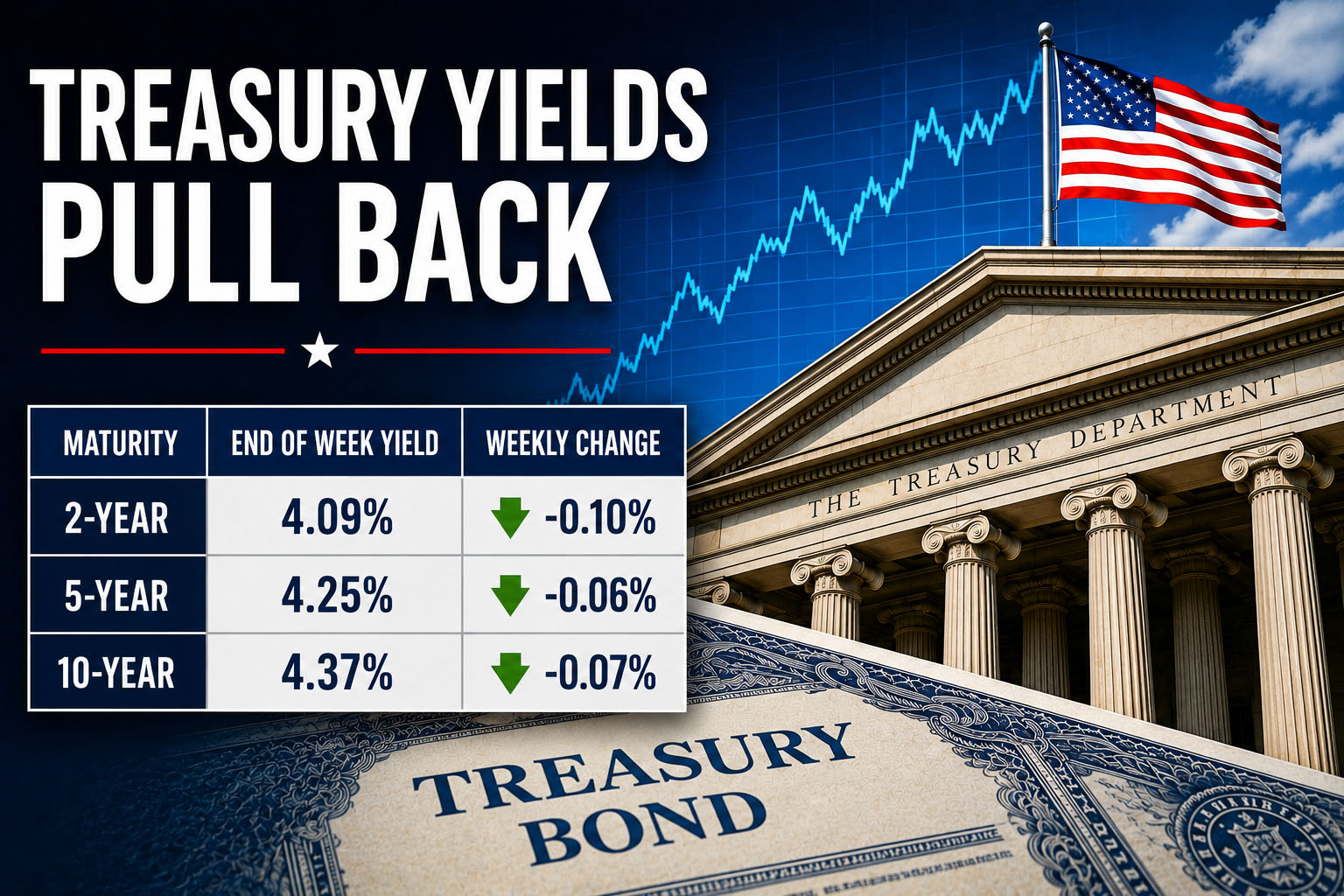

| Maturity | End of Week Yield | Weekly Trend |

|---|---|---|

| 2-Year Treasury | ~4.09% | ↓ Lower |

| 5-Year Treasury | ~4.25% | ↓ Slightly Lower |

| 10-Year Treasury | ~4.37% | ↓ Lower |

The decline was led by shorter maturities after traders reduced expectations for additional Federal Reserve tightening later this year.

What Moved Rates This Week?

1. Middle East Tensions Began to Ease

The biggest driver of rates early in the week was the changing geopolitical landscape.

Only weeks ago investors feared disruptions to global oil supplies that could reignite inflation. As diplomatic developments reduced those concerns, crude oil prices fell sharply.

Lower energy prices immediately reduce inflation expectations.

Because inflation expectations are one of the primary drivers of Treasury yields, bonds rallied and yields moved lower.

2-Year Treasury: Still Focused on the Federal Reserve

The 2-year Treasury remains the maturity most sensitive to expected Federal Reserve policy.

Earlier in the week the yield briefly climbed toward its highest level since early 2025 as markets continued pricing in the possibility of another Fed rate increase. However, by week’s end:

- Cooling inflation data

- Falling oil prices

- Moderating expectations for additional tightening

all combined to push the yield back lower.

The message from the front end of the curve remains clear:

Markets believe the Fed is likely to keep policy restrictive, but investors are becoming less convinced that substantially higher rates will be necessary.

5-Year Treasury: The Middle Ground

The 5-year note sits between short-term monetary policy expectations and longer-term economic growth.

This week it reflected both:

- reduced inflation fears,

- expectations that policy will remain restrictive,

- but increasing confidence that inflation continues to gradually normalize.

The result was a modest decline in yield rather than a dramatic move.

10-Year Treasury: Growth Expectations Moderate

The benchmark 10-year Treasury finished the week around 4.37%-4.40%.

Unlike the 2-year note, the 10-year is influenced less by the next Federal Reserve meeting and more by long-run expectations for:

- economic growth,

- inflation,

- federal deficits,

- and global demand for U.S. government debt.

Investors appeared increasingly comfortable that inflation is moving lower without requiring another major surge in long-term yields.

The Yield Curve Continued to Flatten

One of the week’s most interesting developments was continued flattening of the Treasury curve.

Although both the 2-year and 10-year yields declined by week’s end, shorter maturities remained relatively elevated.

That tells us investors still expect:

- restrictive monetary policy in the near term,

- slower economic growth over time,

- inflation to continue moderating.

Historically, flattening curves often occur late in the economic cycle as financial conditions tighten. Importantly, a flatter curve does not automatically imply recession. Rather, it reflects markets pricing slower future growth relative to current conditions.

Economic Data Driving the Market Next Week

Next week could produce considerably more volatility than the week just ended.

Markets will focus on several high-impact releases, including:

- JOLTS Job Openings

- ADP Private Payrolls

- ISM Manufacturing PMI

- Weekly Initial Jobless Claims

- June Nonfarm Payrolls (released Thursday because of the July 4 holiday)

- Factory Orders

The June employment report will likely be the week’s most important event.

A stronger-than-expected jobs report could push Treasury yields higher by reinforcing expectations that the Federal Reserve will maintain a restrictive policy stance for longer.

Conversely, weaker labor market data would likely encourage additional buying of Treasuries and place downward pressure on yields.

Political and Global Events to Watch

Beyond economic data, investors will also monitor:

- developments in the Middle East and their impact on energy prices,

- discussions at the ECB’s Sintra central banking forum,

- China’s manufacturing data,

- any additional comments from Federal Reserve officials.

Any renewed geopolitical tensions that push oil prices higher could quickly reverse this week’s decline in Treasury yields.

Bottom Line

This week’s Treasury market reflected a meaningful shift in investor sentiment.

The immediate fear of another inflation shock eased as oil prices declined and geopolitical risks moderated. At the same time, investors continued to expect the Federal Reserve to maintain restrictive policy while becoming somewhat less convinced that significantly higher interest rates will be required.

With the June employment report arriving next week, Treasury markets are likely entering one of the most important periods of the summer. Strong labor data could send yields back toward recent highs, while signs of slowing employment growth would reinforce the bond market’s recent rally.

For investors, the message remains the same: the Treasury market is still being driven by the delicate balance between inflation, Federal Reserve policy, and the resilience of the U.S. economy.

Sources

- U.S. Department of the Treasury. Daily Treasury Par Yield Curve Rates. https://home.treasury.gov/resource-center/data-chart-center/interest-rates/pages/textview.aspx?data=yield

- Federal Reserve Board. Monetary Policy and Federal Open Market Committee (FOMC). https://www.federalreserve.gov/monetarypolicy.htm

- Federal Reserve Bank of St. Louis (FRED). Market Yield on U.S. Treasury Securities. https://fred.stlouisfed.org

- U.S. Bureau of Labor Statistics (BLS). Employment Situation. https://www.bls.gov/news.release/empsit.htm

- U.S. Bureau of Labor Statistics (BLS). Consumer Price Index (CPI). https://www.bls.gov/cpi/

- U.S. Bureau of Economic Analysis (BEA). Personal Income and Outlays (PCE Inflation). https://www.bea.gov/data/personal-consumption-expenditures-price-index

- Institute for Supply Management (ISM). Manufacturing and Services PMI Reports. https://www.ismworld.org/supply-management-news-and-reports/reports/

- U.S. Census Bureau. Factory Orders and Durable Goods Reports. https://www.census.gov/manufacturing/m3/

- U.S. Department of Labor. Weekly Unemployment Insurance Claims. https://www.dol.gov/ui/data.pdf

- ADP Research Institute. National Employment Report. https://www.adpemploymentreport.com/

- CME Group. FedWatch Tool. https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

- CME Group. U.S. Treasury Futures Market Data. https://www.cmegroup.com/markets/interest-rates/us-treasury.html

- The Wall Street Journal. Markets, Treasury Yields, and Federal Reserve Coverage. https://www.wsj.com/news/markets

- Bloomberg. Rates & Bonds Market News. https://www.bloomberg.com/markets/rates-bonds

- Reuters. Global Markets and U.S. Treasury Coverage. https://www.reuters.com/markets/

- MarketWatch. Bond Market and Treasury Yield Coverage. https://www.marketwatch.com/investing/bonds

- New York Federal Reserve. Treasury Market and SOMA Holdings. https://www.newyorkfed.org/markets

(Visit Fin Pro Marketing – The Best Marketing for Finance Professionals)

Billy Lee, CEO of Great White Financial, is a sportsman, businessman, artist, speaker, writer, and producer.

Billy is the Founder of the Wellness Institute for Economic Growth and Kairos Athletics.